Anchor Protocol Explained

*This article has been extracted from a report on Anchor Protocol. We briefly examine exactly how Anchor works, and then focus on the risks faced by the depositor.

Executive Summary

Anchor is a protocol on the Terra blockchain network that offers ~20% Annual Percentage Yield (APY) on deposits of UST, Terra’s native stablecoin (TerraUSD) which is pegged to the US dollar.

In other words, it is a savings account that offers ~20% interest.

Interest is paid every Terra block (~7 seconds), there is no minimum deposit amount, and there is no lock-in period. The withdrawal fee is $0.25 USD for any amount, while the deposit fee scales with the deposit amount, to a maximum of $1.90 USD.

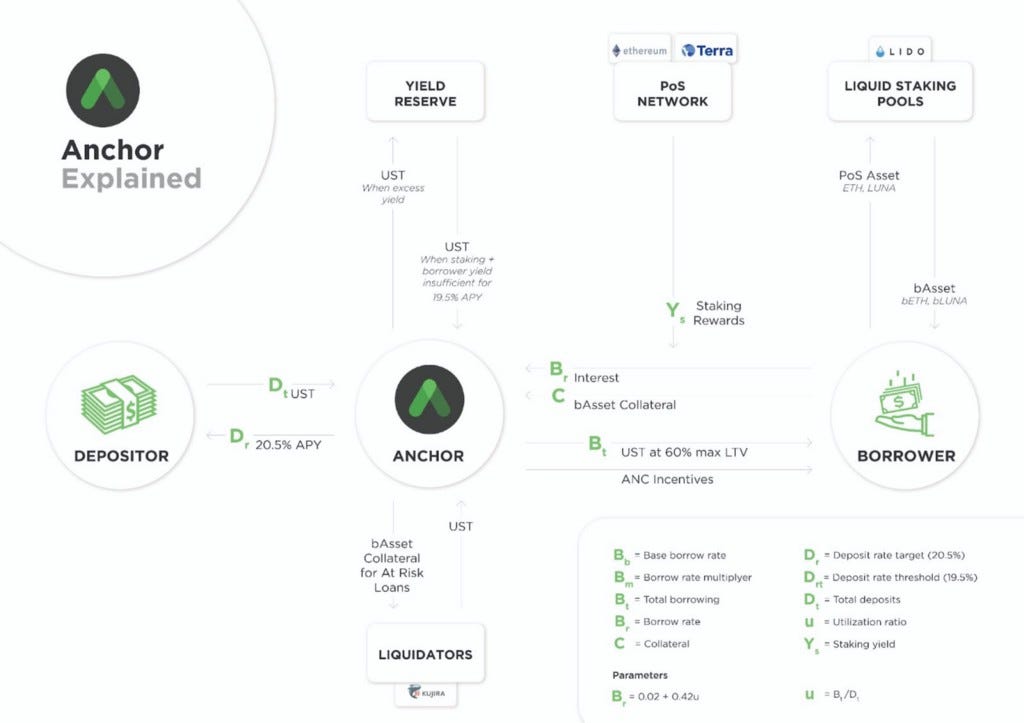

How does it do this? Anchor lends out deposits against overcollateralized digital assets at a variable borrow rate, and only against the yield-bearing assets of major Proof-of-Stake (PoS) blockchains (currently bETH and bLuna).

In traditional finance terms, Anchor is a digital asset money market that only accepts yield-bearing assets as collateral, and uses the yield from those assets to stabilize the interest rate paid out to depositors.

The key risk that depositors take on is that of a crash in the prices of assets used to collateralize loans. Depositors may start to incur losses at sudden declines of more than 40%.

Depositors are also exposed to the risk of the peg between UST and USD becoming unbound, as well as that of a lack of liquidity for liquidations of at-risk collateral, allowing loans to become undercollateralized. Given that Anchor is less than 12 months old, there is also uncertainty around the long-term sustainability of the Anchor model, especially at a depositor APY of 20.5%.

All of the risks inherent in any cryptographic protocol are also present: all smart contract risks, wallet risk and hacking risk.

For those that do not use USD as their native currency, using Anchor will also incur forex risk.

As of January 2022, Anchor has seen inflows of ~$10 billion USD in total deposits and collateral, has not suffered any major exploit or hack, and has maintained an APY > 17% for the duration of its lifespan (~10 months).

What is Anchor?

Introduction

Anchor is a decentralized savings protocol built on the Terra blockchain network. Described as the ‘Gold Standard for Passive Income on the Blockchain,’ Anchor was first introduced to the world in a June 2020 white paper, and launched on March 17, 2021. Since then, Anchor has attracted $10 billion USD in total value, with ~$5 billion in deposits and ~$5 billion in collateral.

Anchor aims to provide a household savings product in the crypto markets with the following features:

Stable interest rate, by accepting only yield-bearing assets as collateral and passing on block rewards of Proof-of-Stake (PoS) blockchains to depositors as a stabilization mechanism

Principal protection, through the use of a liquidation protocol that automatically liquidates borrower collateral when a loan is at risk

Widespread accessibility, with no minimum deposit amounts, no lock-in period, minimal deposit and withdrawal fees, and the ability to accept deposits from anyone, anywhere

In addition to providing a low-volatility, high-yield product, Anchor also has the potential to become a core building block of the decentralized financial system:

…Anchor is an attempt to give the main street investor a single, reliable rate of return across all blockchains. By aggregating block rewards from all major PoS blockchains, Anchor aspires to set the blockchain economy’s benchmark interest rate.

How does it work?

From Anchor’s white paper:

To generate yield, Anchor lends out deposits to borrowers who put down liquid-staked PoS assets from major blockchains as collateral (bAssets).

Anchor stabilizes the deposit interest rate by passing on a variable fraction of the bAsset yield to the depositor. It guarantees the principal of depositors by liquidating borrowers’ collateral via liquidation contracts and third-party arbitrageurs.

The core mechanics of Anchor are relatively simple.

Depositors lend Anchor UST (the Terra network’s USD stablecoin) in exchange for stable yields.

Borrowers borrow UST from the deposit pool, locking up yield-bearing bonded Assets (bAssets) of major Proof-of-Stake blockchains as collateral, and paying an interest rate to do so.

Anchor pays depositors yield from two sources: interest paid on borrowings and staking rewards from the collateral.

Excess yields are sent to the yield reserve to be distributed in the future, when yield inflow does not cover yield outflow.

Key components

Let’s break down some of these basic components.

A stablecoin is a cryptocurrency that is designed to hold a stable value, usually that of $1 USD. Depending on the method used to peg the value of a stablecoin to the USD, they are considered to be relatively risk-free.

The stablecoin used in Anchor is TerraUSD (UST), the native USD-pegged stablecoin of the Terra ecosystem.

A Proof-of-Stake blockchain is a blockchain network that uses a consensus mechanism known as ‘Proof-of-Stake’ to validate transactions. Without going into too much detail, ‘staking’ involves locking crypto-assets into a cryptocurrency protocol to participate in the validation process to add new blocks to the blockchain.

In Proof-of-Work (PoW) blockchains such as Bitcoin, the equivalent process is known as ‘mining,’ and involves a computationally intensive process. Miners are rewarded with Bitcoin for their efforts in securing the network.

Similarly, stakers in PoS blockchains are rewarded for their efforts with emissions (new supply) of the native token of the blockchain (i.e. ETH for the Ethereum blockchain, Luna for the Terra blockchain).

Because the process of securing the blockchain must have an economic cost, staking carries the risk of loss of the staked tokens. Further, there may or may not be a lock-up period associated with the withdrawal of tokens from a ‘staked’ state.

A bAsset or Bonded Asset is a derivative asset that represents a claim on a staked amount of a blockchain’s native token. As described above, staked assets earn ‘staking yield,’ that is, rewards in return for securing a blockchain’s transactions.

Like the underlying staked asset, a bAsset pays the holder block rewards. Unlike the staked asset, a bAsset is both transferable and fungible, and can therefore be used in the wider DeFi ecosystem.

As of January 2022, Anchor only accepts bETH and bLUNA as collateral. bLuna makes up more than 90% of the current value of deposited collateral.

Participants

There are a number of core parties in the Anchor money market:

The Anchor protocol, a series of smart contracts that facilitate the money market.

Depositors, who provide liquidity to Anchor in exchange for a stable yield.

Borrowers, who deposit bAsset collateral to Anchor to borrow UST. Borrowers can gain access to liquidity without having to sell their bAsset.

bAsset liquidity providers, who turn illiquid staked assets into liquid derivative claims on those assets (bAssets)

Liquidators, who monitor and bid on at-risk loans and purchase liquidated collaterals.

Anchor (ANC) token holders, who are able to create and vote on proposals that govern the core parameters of Anchor.

TerraForm Labs, the company behind the Terra blockchain network.

Oracle feeders, a smart contract that acts as the price source for the Anchor Money Market. Stablecoin-denominated prices of bAssets are periodically reported by oracle feeders.

Mechanics

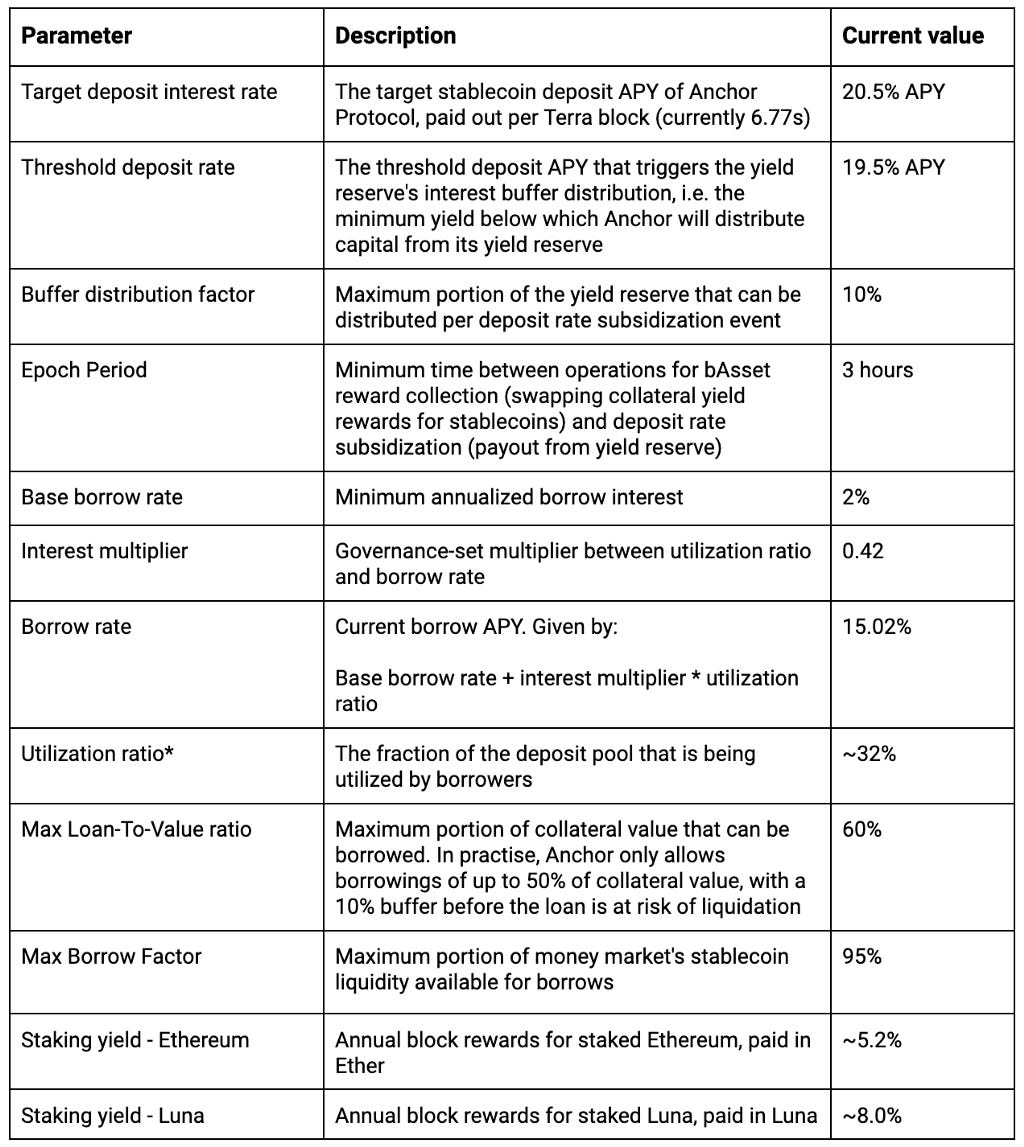

Money market parameters

As with any money market, there are some basic parameters that define the system. All of the parameters are set by Anchor Governance (holders of the ANC token).

* Not set by Anchor Governance.

The Anchor Money Market

Let’s take a look at what these numbers mean in practice.

From Anchor’s dashboard (Jan 08, 2022):

Total Deposits $5.3b

Total Collateral $4.8b

bLuna $4.3b (60.9M Luna)

bETH $0.46b (0.14M ETH)

Total Borrows $1.8b

Yield Reserve $63.0m

Given Anchor’s current target APY of 20.5%, the protocol must generate just under $1.1b in annual yield:

$5,300,000,000 * 20.5% = $1,086,000,000

Total deposits * target APY

The interest on loan positions generates $273m in yield towards this:

$1,800,000,000 * 0.152% = $273,000,000

Total borrow * borrow APY

Block rewards from collateral generates an additional $364m in yield:

60,950,000 * 8.0% * $70 = $341,00,000

Number of Luna * Annual reward rate * price of Luna

142,000 * 5.2% * $3,200 = $23,600,000

Number of ETH * Annual reward rate * price of ETH

Note that the dollar-denominated value of the block rewards depends heavily on the current price of the token (Luna, ETH), and therefore will fluctuate significantly.

Total APY generated:

$273m + $341m + $23.6m = $638m

So Anchor is currently seeing a deficit of $448 million per year at current inputs.

The Threshold Deposit Rate is the rate at which Anchor will start to use its yield reserve to augment yield to depositors.

With $638m being distributed to $5.2b in deposits, we get an annual yield (without the yield reserve) of 12.20%, which is below this threshold.

Therefore in this case, the yield reserve will top up the APY for depositors, at maximum once every three hours (limited by the Epoch Period).

In the case where there was an excess of yield, the surplus would be added to Anchor’s yield reserve to be distributed at a later date.

Debt positions

Let’s take a look at a debt position in Anchor.

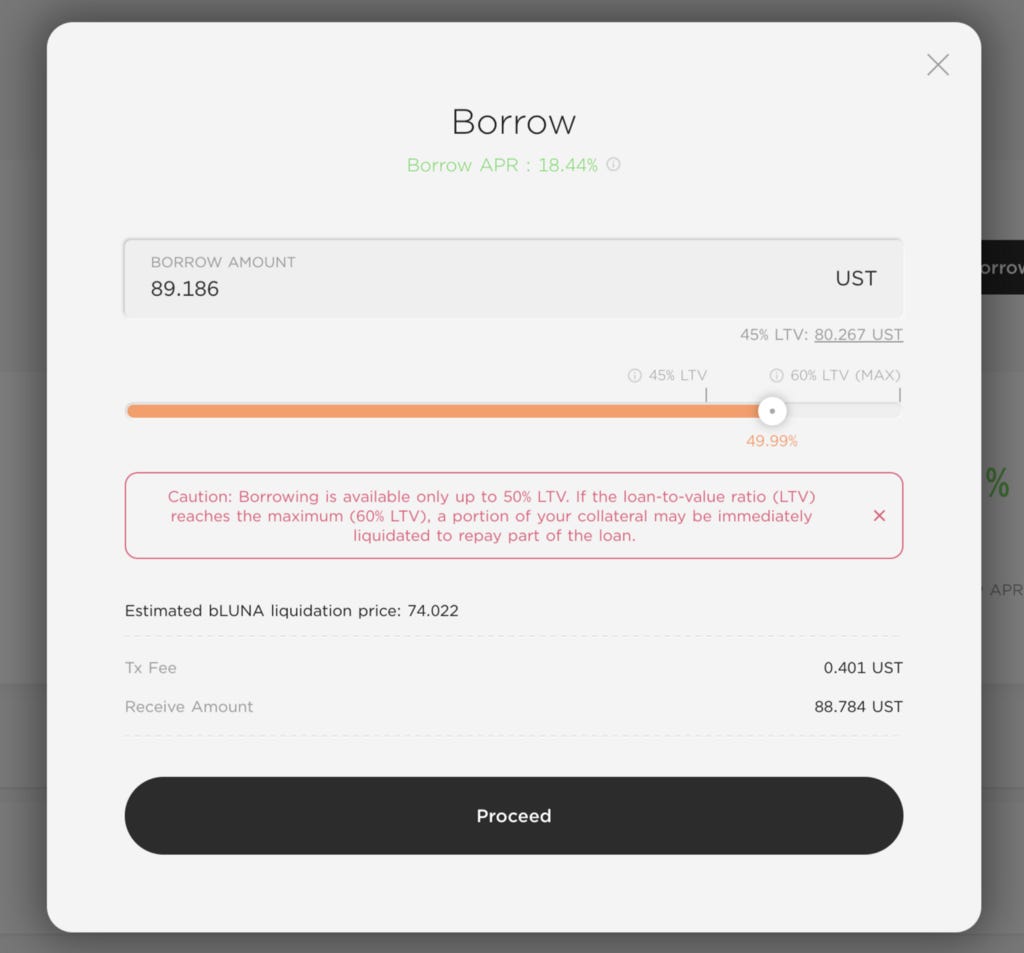

The main parameter of a debt position is its borrowing capacity, or the maximum amount of debt an account can borrow. The current max LTV (Loan-to-Value ratio) is 60% for both accepted types of collateral, bLuna and bETH. Anchor currently only accepts overcollateralized positions.

Therefore an account that deposits 10 bETH would have a maximum borrowing capacity of 6 ETH worth of UST, with the USD-denominated value of this position fluctuating with changes in the price of Ether.

Combinations of collateral are also accepted by Anchor. For example, an account that has deposited 10 bETH and 10 bLuna would have a borrowing capacity equal to the USD value of 6 ETH + 6 Luna.

As we can see in the market parameters, the interest rate on borrowing is a function of utilization ratio, or how much of the deposit pool has been lent out. Currently, the borrow rate sits at 15.02%.

As the utilization rate increases, the interest rate increases, thus incentivizing repayment. Similarly, when utilization is low, borrowing is incentivized with lower interest rates.

Anchor’s white paper details why this model alone is insufficient to provide a stable interest rate to depositors. See the appendix for more details.

There is a reasonable question here about who the borrowers of Anchor are. Why pay interest to borrow money when you have at least 167% of the amount you can borrow?

The answer has to do with leverage. The bAssets used as collateral in Anchor are highly speculative assets with potentially large upside. Thus, Anchor allows a user to maintain exposure to these assets while also being able to make use of the locked value as collateral to invest elsewhere. 18% may be too high a hurdle for traditional assets, but in cryptocurrencies this can be simply daily volatility.

ANC incentivization

It is also important to note that for the duration of Anchor’s lifespan so far, all borrowing has been incentivized by the emission of Anchor (ANC) tokens. Starting at 340% APY when Anchor was launched, to stabilizing at ~15% APY in Jan 2022, borrowing money from Anchor has until recently actually had a net positive yield.

Here’s an example of how this worked:

Deposit $1,000 USD worth of bAsset collateral into Anchor

Borrow $400 UST to invest elsewhere

APY on the borrowed UST is ~18%, payable in stablecoins

However, due to ANC incentives, the borrower would be receiving (for example) 100% APY of the borrowed amount in ANC tokens

The borrower could then sell those ANC tokens after paying back the loan, to have a negative cost of borrowing (that is, they make a profit for borrowing from Anchor)

Obviously the true APY is dependent on the price of the ANC token at the point of sale, and so borrowing in this manner takes on an additional risk in the form of exposure to ANC. However, because the price of ANC can not be negative, it means that the most the borrower would pay would be 18% (the cost of borrowing) and in most cases it would be much less than this.

While it is not necessary to fully understand the mechanics of the ANC token to understand how Anchor works, we have included a few notes in the Appendix at the end of this article.

Liquidations

In order to protect the principal of depositors, Anchor needs a robust liquidation mechanism to enforce its 60% max LTV. Depositors are safe as long as all debts are overcollateralized.

Rather than relying on open market liquidity for the collateralized assets, Anchor actively incentivizes liquidators to observe and liquidate unsafe loans through the use of ‘liquidation contracts.’

A liquidation contract is a standing bid on bAsset collateral, capitalized by locked UST. They can be submitted by anyone through Anchor’s liquidation queue, Kujira, are aggregated in a pool and tapped ‘on demand’ when a loan is at risk.

The advantage of this approach is that liquidity for liquidations is predictable, stable and public. We can see that there is currently $59 million in liquidation bids capitalized and ready to provide liquidity for at-risk debt positions.

Loans with a total collateral value of above 2,000 UST are partially liquidated, with only a portion of collateral liquidated instead of liquidating the full amount. Below 2,000 UST, locked collaterals are fully liquidated.

Here is a simple example of how the liquidation contract system works.

Alice opens a debt position on Anchor by depositing 100 bLuna at a price of $100.

She borrows 5,000 UST. Her LTV is thus 50%.

The price of Luna drops to $80.

The LTV of Alice’s debt position is now 62.5% ($5,000 in debt collateralized by $8,000 in bLuna) and her position is now at risk.

Bob has submitted a liquidation contract in Kujira, to buy bLuna at a 5% discount. He capitalizes this bid with $10,000 UST.

Because Alice’s position is above the maximum allowed LTV, Anchor taps the liquidation queue for the best liquidation contract. Assuming that Bob’s position is the only open contract, his bid will be filled for $5,000 UST.

Anchor will use this $5,000 in UST to repay Alice’s debt, making depositors whole.

In return, Bob receives $5,000 of Alice’s bLuna at a 5% discount* — i.e. he will receive 65.7 bLuna (market value $5,256).

Alice’s position in Anchor after her loan has been liquidated will show 34.4 bLuna.*

*We have simplified this explanation slightly. The liquidator will receive an additional liquidation fee of 1% of the total value of collateral, as does Anchor, so the actual amount will be slightly less.

Analysis of depositor risks

Risks of permanent loss

In order to fulfill its goal of being the ‘household savings product powered by cryptocurrency,’ Anchor must provide stable, low-volatility yield with minimal risk. However, unlike an FDIC-backed checking account, Anchor deposits are not insured, and it is far from risk-free. There are a number of scenarios where depositors will bear permanent losses.

UST peg becomes unbound

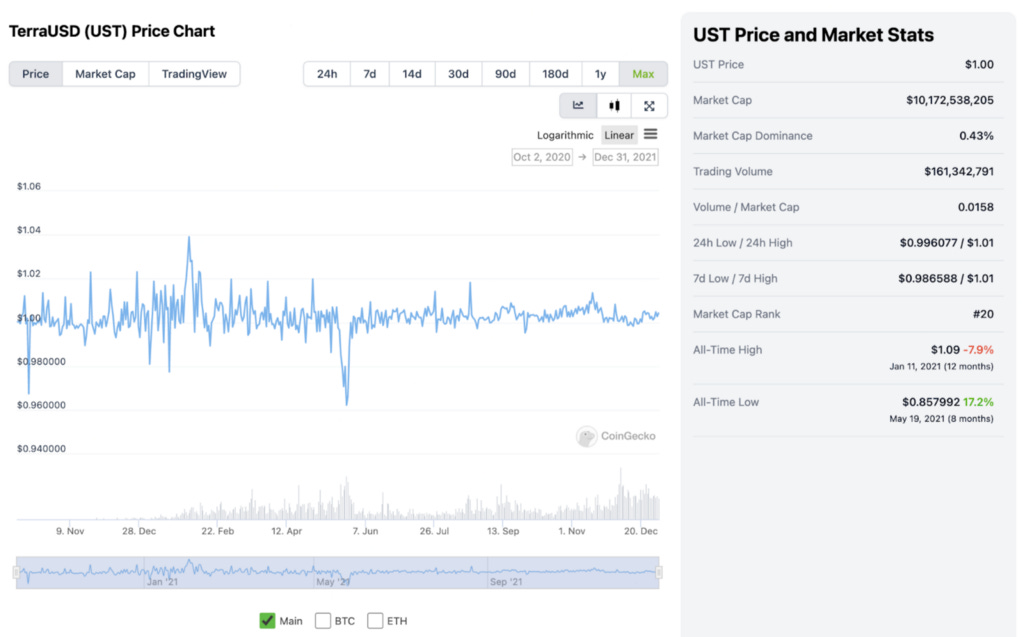

UST is the native stablecoin of the Terra ecosystem, and is designed to maintain a tight peg around $1 USD.

All deposits in Anchor are affected by changes in the value of UST. As of Jan 2022, there is ~$10 billion UST in circulation. As we can see on the price chart, there have been fluctuations of ~4% both ways in its short lifespan so far.

During the May 2021 cryptocurrency crash, the price of UST fell to $0.96 USD and remained below $1 for nearly a week before recovering. Since then, it has exhibited relative stability under ordinary conditions.

How does the UST peg work?

UST is pegged to $1 USD through a simple mechanism: the Terra network’s algorithmic market module will always swap Luna (the Terra network’s native coin, the equivalent of ETH on the Ethereum network) for UST at the network’s target exchange rate, i.e $1 USD = 1 UST.

This incentivizes users to maintain the price of UST through a riskless arbitrage opportunity.

When 1 UST > 1 USD, users can trade 1 USD of Luna for 1 UST. The market burns 1 USD of Luna and mints 1 UST. Users can then sell their 1 UST on the open market for a riskless profit, increasing the supply of the UST pool. The arbitrage continues until UST price falls back to match the price of USD, maintaining the peg.

The same arbitrage mechanism works in reverse for contraction.

Insurance can be bought through a protocol called Unslashed for this depegging risk, however this is only relevant if UST is trading below 0.87 UST per USD, a much larger discrepancy than has ever happened.

Smart contract risk

All blockchain protocols are simply a set of smart contracts programmed to follow a specific set of rules. As with any program, they are susceptible to errors and vulnerabilities in the code. Smart contract risk is the risk that an attacker finds a way to drain, divert or otherwise misappropriate value locked inside a protocol.

The worst case scenario for Anchor is that depositors’ funds are drained from the treasury, resulting in permanent loss.

While difficult to quantify, we can have some confidence that the smart contract risk for Anchor is relatively low, due to the following:

Third-party audit reports for all core deployed Anchor code

An ongoing, globally available bug bounty program with rewards up to USD $1.05m

The lack of critical failures so far, eleven months into Anchor’s existence, with ~$10 billion in funds at risk (one of the top ten largest protocols by total value locked, making it a particularly attractive target)

The test of time is perhaps the best indicator for the robustness of a smart contract, assuming there are no new developments that might introduce new vulnerabilities.

Composability risk

Composability is the property of a platform that allows its existing resources to be used as building blocks for new systems. For Anchor, this means integrations with other protocols.

New interactions between Anchor and other protocols introduces an additional vector for smart contract risk.

A number of decentralized insurance protocols (Unslashed, Bridge Mutual) offer insurance against smart contract risk on Anchor, at rates of around 6% per year.

bAsset price crash (>40%)

As Anchor is an overcollateralized lending market, the safety of depositors’ capital is dependent on the value of the underlying collateral, bLuna and bETH.

The closer the effective LTV ratio of the overall Anchor portfolio becomes, the more risk is borne by depositors.

Anchor’s maximum allowed LTV is 60%, above which borrowers are at risk of liquidation. How likely is it that bAsset prices suddenly collapse by 40% or more, leaving borrowers undercollateralized and depositors with exposure to bAsset prices?

(Given that more than 90% of collateral in Anchor is currently bLuna, we will focus on the price movements of Luna).

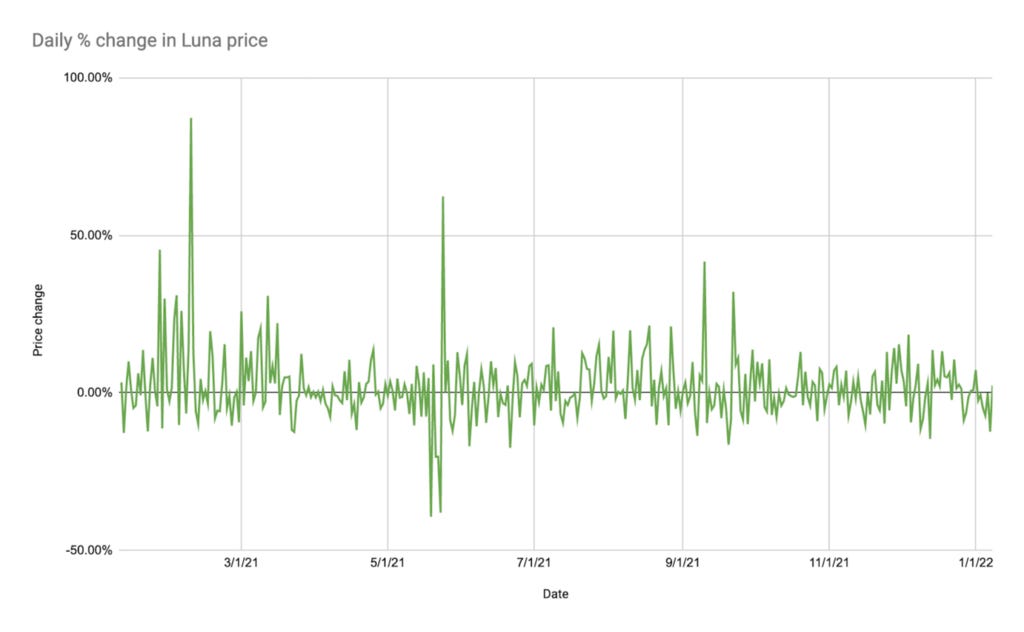

We can see a number of sudden declines, against the backdrop of a bullish run for Luna in 2021. What we want to see is the magnitude of the declines in terms of a percentage drop.

Graphing the daily price change against time, we get:

On 19 and 23 May, Luna price dropped 39% and 38% from the previous day’s close. This coincided with a broader crash in the cryptocurrency market, with BTC falling nearly 50% from $58,000 to $34,000 in the month of May.

Given the historical volatility of the cryptocurrency market, it would be unreasonable to assume that a drop of this magnitude can not happen again.

This risk of a crash in the value of collateral is a fundamental risk of depositing money into Anchor.

While the recent price drops look to be larger, on a percentage basis they are relatively small — between 9% to 14% for the most significant drop in early 2022. Luna’s volatility for 2021 was 2.09, compared to 0.8 for BTC.

While it may seem to be relatively low-risk, Anchor is still indirectly correlated with the overall health of the cryptocurrency market — albeit with a relatively large cushion. Anchor protocol’s LTV ratio provides a buffer between the depositor and the cryptocurrency market, providing stable, fixed yield under all conditions apart from a market crash.

For clarity, here is how a crash in bAsset prices causes losses for depositors:

Price of bLuna drops sharply on open market

LTV limits of a large number of loans will be breached, putting them at risk of liquidation

Liquidation contracts will be activated and likely very quickly exhausted (the current ratio between active liquidation bids and outstanding loans is 3.5%)

As the price drops, more and more loans will breach the allowed LTV and be at risk of liquidation

Because the liquidation pool has been exhausted, bids for bLuna collateral will be accepted at high discounts to the market price

This will likely cause the market price to drop further in a cascading liquidation cycle, as liquidators buy bLuna, swap it for Luna, then sell this on the open market

In addition, once existing liquidation bids have been fully exhausted, at-risk loans will simply be held by Anchor, which has no recourse to liquidate the collaterals.

Thus, depositors will start to gain increasing exposure to bAsset prices.

Once loans become undercollateralized — that is, the value lent out is more than the value of the collateral provided — borrowers have no incentive to repay loans, and the loss in value is borne by depositors.

While price crashes expose depositors to the risk of loss, slow price declines do not. The reason for this is because in a decline, the number of debt positions breaching their max LTV ratios increases slowly and liquidation bids are unlikely to be overwhelmed. A slow decline also allows the market more time to respond, and thus for liquidators to replenish their bids, keeping the system intact.

Insufficient liquidation contracts

Anchor relies on third-party liquidators to liquidate at-risk loans. They are provided with strong financial incentives to do so (1% liquidation fee, discount to market price), however given the relative immaturity of cryptocurrencies and market inefficiencies, it is not impossible that for whatever reason, there are not sufficient liquidation bids for at-risk loans.

The effect of this would be that Anchor will hold debt above the maximum allowed LTV ratio for an extended period of time, increasing asset price exposure to depositors, until enough liquidation bids are submitted to liquidate all at-risk loans.

While one of the advantages of a decentralized system is that anyone can participate, this can also be a disadvantage — no one is obligated to participate

Anchor is a Ponzi scheme

How do we know that Anchor is not simply a digital asset ponzi scheme? We can see deposit, borrow and collateral numbers on the Anchor web app, but how do we know this is accurate until a liquidity crunch?

One of the fundamental mechanics of a blockchain network is that transactions must be broadcast publicly, to the entire network, to be validated. What this means in terms of assessing Anchor’s validity is that we can see, independent of the Anchor web app, that the values shown for total deposits, collateral, borrows etc, are accurate.

For example, we can see the currently available liquidity here, and the bLuna collateral here.

See Anchor deployed smart contracts for more.

Bank run

A bank run is when ‘a large number of customers of a bank or other financial institution withdraw their deposits simultaneously over concerns of the bank’s solvency.’

Because Anchor’s lending activity is overcollateralized under normal conditions, this definition is not relevant to Anchor except in the case of a price crash in the collateral used to back Anchor’s loans.

This risk has been discussed above, however we can simulate a large coincidental volume of withdrawals under normal conditions.

Anchor’s current utilization rate is ~32% — that is, roughly 32% of the stablecoin deposits have been lent out to borrowers.

What happens when 80% of depositors suddenly want to withdraw their capital?

The documentation offers no guidance for this, but we can assume that the first 68% of depositors will be able to be paid out from liquid reserves.

As this is happening, two of the underlying parameters that govern Anchor come into play.

Borrow rate increases. The interest rate charged to borrowers is a function of the utilization of the deposit pool. As deposits are withdrawn, the effective utilization increases, increasing the borrow rate to a maximum of 40%. This disincentivizes new loans and incentivises repayment of existing loans.

New debt positions will not be able to be opened. The maximum utilization is set at 95% of the deposit pool.

What happens to the other 12% of depositors that want to withdraw their capital?

Once the reserves are depleted, there is no liquidity left. In the scenario where there are no underlying issues with the Terra ecosystem or Anchor’s collateral value, we expect that depositors will be able to withdraw their capital over time as loans are paid back and new depositors enter the market.

A quick look at the smart contract code governing withdrawals seems to indicate that there are no unusual provisions for a scenario like this, so we assume that deposits will be processed chronologically until there is no liquidity left, at which point deposit requests simply return an error until more liquidity becomes available.

Risk of inadequate return

Anchor has been in operation for less than a year. While it is an incredible innovation, the long-term sustainability of its model is still in question, especially given that 20.5% yield on a stablecoin is much higher than that of its digital asset competitors, and stratospherically higher than yields offered in traditional financial products.

Anchor model unsustainable

The biggest question to be asked is if Anchor’s model can sustainably generate 20.5% yield on average for depositors from bAsset block rewards and borrower interest.

We believe that Anchor’s long-term sustainability will depend on its ability to balance growth in deposits with growth in borrowings. Further, we believe that it is highly probable that the target deposit rate will either decrease or become variable in the near future.

While we cannot provide a definite answer, here are a few points to consider:

The Anchor model is currently skewed towards incentivizing deposits: the borrow rate is variable based on the utilization ratio, but the deposit rate is fixed. The issue with this is that Anchor must be able to generate borrow demand at whatever rate deposits increase, with no lever to slow down deposits.

While we have very little historical data, Anchor was launched just prior to the May 2021 cryptocurrency crash. While BTC fell nearly 50%, Anchor deposits took a small 7% hit before resuming a steady increase. Given this, and the fact that Anchor offers stable returns, it seems reasonable to assume that deposit demand will increase in a bear market.

This would need to be followed by an equal increase in borrowings, however we know from historical data from other digital money markets that borrowing activity falls in a bear market (speculative activities see an overall decrease).

Thus, Anchor needs to build up its yield reserve in bull markets, in order to be able to maintain deposit APY during bear markets.

The yield reserve*, which peaked at ~$79m on Dec 11, 2021, has been steadily decreasing at ~$500,000 per day since following a large uptick in deposits in December, including a ~$550m increase on Dec 21. The deposit APY has fallen to its threshold minimum of 19.5%, which it has maintained since then.

Borrowing needs to increase by ~$400m in order for equilibrium to be reached.

At the current rate, the yield reserve is able to sustain deposit APY for 140 days, or roughly five months.

All of the above signal a need to either limit deposit growth or reduce deposit APY in some way, in lieu of being able to rapidly incentivize demand for borrowing.

*A note on the yield reserve: in Jul 2021, TerraForm Labs capitalized the reserve with a one-time $70 million infusion, in order to give Anchor a significant runway to reach sustainability. Unfortunately, this large reserve did not come from normal operations.

bAsset price and staking exposure

The dollar-denominated value of staking rewards that Anchor collects from bAsset collateral depends on the price and average staking yield of the underlying assets, and is central to the sustainability of Anchor’s model.

A decrease in either will result in lower yield for Anchor, with increased borrow APY needed to sustain depositor APY (all else held equal). All of the variables — Luna price, ETH price, Luna yields and ETH yields exhibit considerable volatility.

While a comprehensive discussion of the future of dollar-denominated Ethereum and Luna yields would be longer than this entire report, it is important to note that the success of Anchor Protocol depends on the survival and development of the wider blockchain ecosystem, and in particular the success of the Luna ecosystem and token.

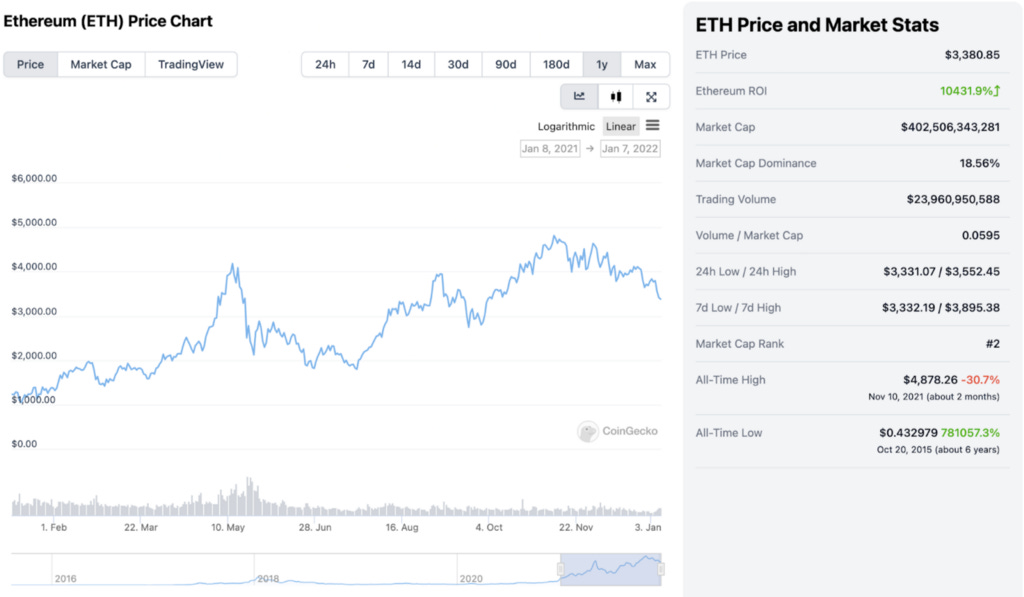

We have examined Luna prices above. Ethereum prices are shown below, with a 2021 volatility

of 0.97.

Ethereum staking rewards are inversely correlated with the number of ETH staked, and offer a current staking yield of ~5%.

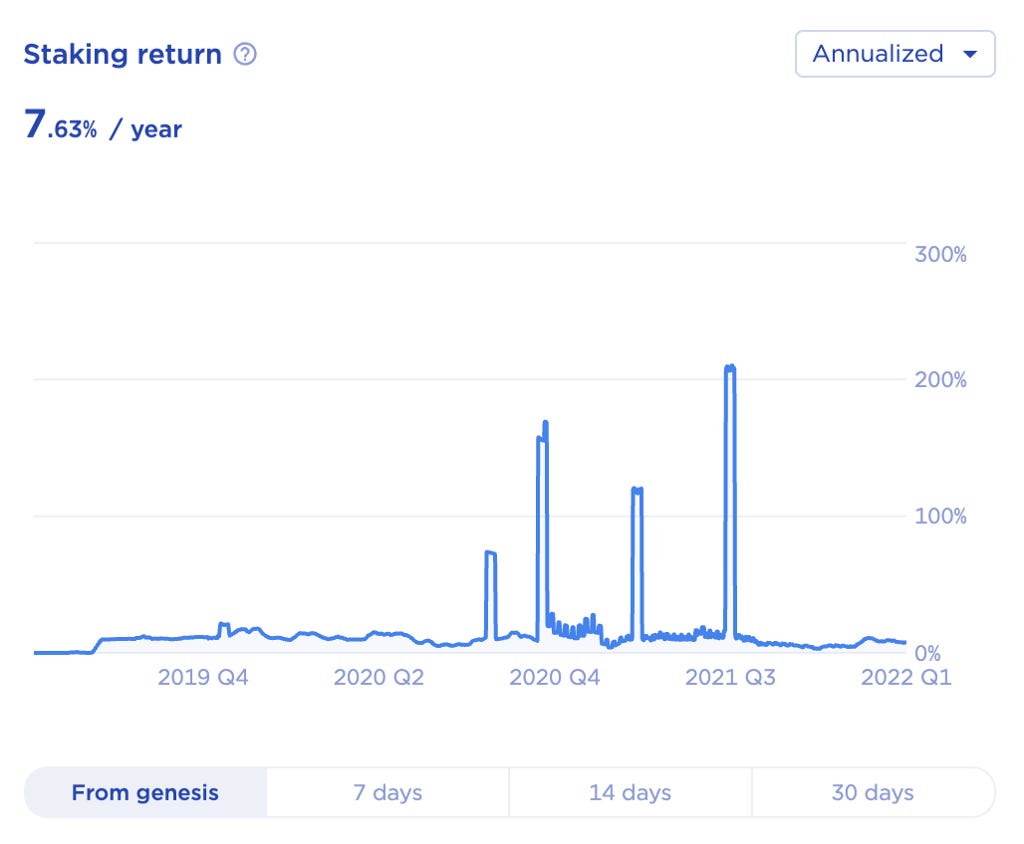

Luna staking yields have historically been highly variable. The large jumps shown below are due to ‘airdrops’ — tokens of new protocols sent to wallets that were staking Luna at the time. These airdrops immediately trade on the open market and thus can be valued in dollar terms, which is what is reflected in the graph below.

Over the longer term and under normal circumstances, the staking yield of Luna depends on two factors: aggregate transaction fees on the Terra network, and the percentage of Luna supply that is staked.

While dated, this report by one of the original authors of the Terra white paper provides a framework for analysis.

Alternative digital asset markets

Anchor is currently the largest digital asset money market on the Terra network, but there are a number of large competitors on the Ethereum blockchain: Aave, Compound and Maker being the main ones.

They also offer borrowing against a variety of digital assets, and while they do not yet support bLuna as a collateral asset, cross-chain interoperability is an increasing trend. Other protocols accepting bLuna as collateral is likely to put downward pressure on Anchor’s borrow rates as well as reducing market share (currently 100%).

More broadly, Anchor’s sustainability is likely to be strongly correlated with growth in the Terra ecosystem, as increases in the price of Luna are likely to increase borrow demand against bLuna.

There do not seem to be any competitors to Anchor on the deposit side, which is positive for the growth of Anchor overall, but potentially negative for sustainability.

Governance changes

Anchor’s core money market parameters are set through governance. ANC tokenholders can propose changes to parameters, which are then voted on and executed on-chain (see example here).

ANC tokenholders could vote to reduce deposit APY from its current target of 20.5%, impairing expected depositor returns.

Other risks

These are risks that are not specific to Anchor, but are risks that are inherent in the use of any blockchain protocol.

Wallet risk

Losing a wallet’s private key (password) or seed phrase is one of the most common forms of risk when dealing with cryptocurrency assets. As wallets are non-custodial, there is no ‘central administrator’ available to ‘reset password’ or otherwise recover lost funds.

Once a wallet’s password details are lost, the funds in the wallet are effectively lost forever.

User error

Like all new technologies, dealing with cryptocurrency transactions can take a little bit of getting used to. User error — in token transfers, authentication and otherwise — can result in lost or misplaced funds.

Again, in non-custodial situations, errors are unforgiving — lost funds are likely lost forever.

Hacking risk

Stories of digital asset wallets being hacked and millions of dollars being stolen are more commonplace than ever. A report by CNBC estimated that cryptocurrencies worth $3.2 billion was stolen in 2021 alone. Because each user is effectively responsible for their own security with non-custodial wallets, they can be attractive targets for hackers.

Anyone with the private key or seed phrase for a wallet has full access to the funds held in that wallet. Software (‘hot’) wallets are vulnerable to attacks on the user’s device, whereas hardware (‘cold’) wallets are more difficult to attack.

We recommend following standard security measures, ideally through a paper wallet or hardware wallet.

Unknown unknowns

While we are confident that significant failures of Anchor will fall under one (or more) of the above risk factors, it would be foolish to assume that we have imagined every possibility. So we leave open the possibilities for unknown unknowns, risk factors that we don’t know we don’t know.

Summary of risks

We consider risks from the perspective of a depositor with native currency USD expecting stable returns averaging 20.5% per annum.

Permanent loss

UST fails to hold its peg to USD, resulting in permanent impairment of capital

The Anchor Smart Contract is hacked, resulting in permanent loss of funds

The Smart Contract of Anchor partners (Lido, Kujira etc.) is hacked, resulting in vulnerabilities in Anchor and permanent loss of funds

bAsset prices crash more than 40%, resulting in undercollateralized positions where the loss is borne by the depositor

There is insufficient demand for liquidation contracts on at-risk Anchor positions, resulting in undercollateralized positions and eventually real losses borne by depositors

Inadequate return

The Anchor model is not sustainable at 20.5% target APY, and is lowered by governance to a fixed number less than 20.5%, or to a variable model

bAsset prices and/or bAsset staking fall, resulting in lower available yield for depositors and inability for Anchor to sustain 20.5% APY

The yield reserve is depleted, and the APY falls to what can be sustained by ongoing borrow interest and bAsset block rewards

Competitor protocols arise that offer better rates on bAsset borrowing, reducing usage of Anchor

Other risks

Wallet risk

User error

Hacking risk

Unknown unknowns

References

Anchor White Paper

https://www.anchorprotocol.com/docs/anchor-v1.1.pdf

Terra White Paper

https://assets.website-files.com/611153e7af981472d8da199c/618b02d13e938ae1f8ad1e45_Terra_White_paper.pdf

Terra Money Medium Article — Introducing Anchor https://medium.com/terra-money/introducing-anchor-25d782cbb509

Anchor Governance parameters

https://docs.anchorprotocol.com/protocol/anchor-governance/modify-market-parameters

Coinlist interview with Do Kwon, Founder of TerraForm Labs

https://blog.coinlist.co/a-deep-dive-into-terra-and-anchor-the-reliable-savings-protocol/

Anchor Deployed Smart Contracts

https://docs.anchorprotocol.com/smart-contracts/deployed-contracts#terra-usd-market-smart-contracts

Terra Money: Analysis of Luna Staking Rewards

https://agora.terra.money/t/analysis-of-luna-staking-rewards/52

Appendix

Utilization

The below is an excerpt from Anchor’s white paper.

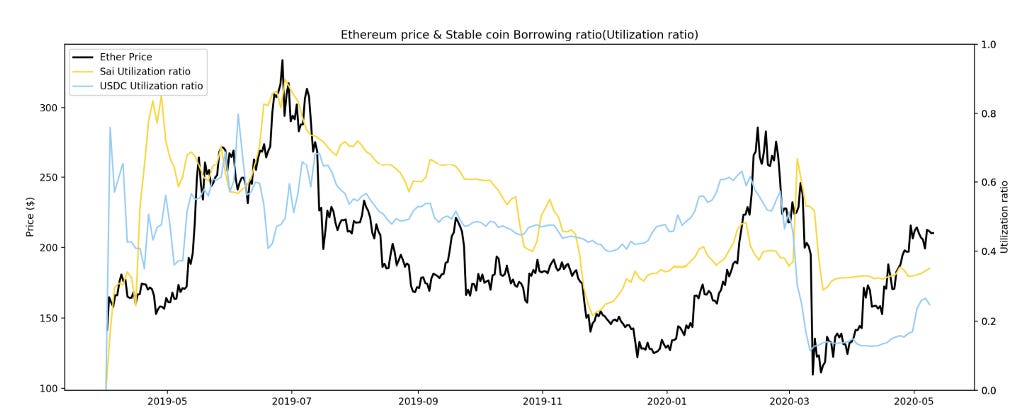

This formulation has a key shortcoming — one that is shared by the Compound protocol which first introduced the idea: both rates are increasing functions of the utilization ratio, and therefore both are highly sensitive to market cycles. A pattern that emerges clearly from historical data on Compound is that the utilization ratio on stablecoin money markets is highly correlated with Ethereum price movements.

Upswings in Ethereum’s price increase demand for leveraged long positions on Ethereum, which results in increased borrowing from stablecoin money markets. The opposite is true during Ethereum price downswings: a decrease in leveraged long demand, in combination with liquidations of Ethereum debt positions, results in less stablecoin borrowing.

The interest rate equations demonstrate that cyclicality in utilization ratio directly translates to cyclicality in borrower and depositor rates. We believe that cyclicality of interest rates on DeFi protocols is a key barrier to broad adoption.

Utilization ratio on stablecoin money markets on Compound is highly correlated with Ethereum price movements. The graph above shows Sai and USDC money market utilization ratios vs Ethereum price over the last 12 months.

The Anchor token

The Anchor Token (ANC) is a cryptocurrency token that serves as Anchor Protocol’s governance token.

ANC tokens can be deposited to create new governance polls, which can be voted on by users that have staked ANC.

ANC is designed to capture a portion of Anchor’s yield, allowing its value to scale linearly with Anchor’s assets under management (or more specifically, the value of bAssets it has accrued as collateral).

ANC tokens generate a buying pressure that increases proportionally with Anchor’s AUM. Protocol fees are used to purchase ANC tokens from Terraswap, which are then distributed as staking rewards to ANC stakers. The source of funds to purchase ANC comes from protocol fees, which are a combination of bAsset rewards, excess yield, and collateral liquidation fees (1%).

ANC is also used as an incentivization mechanism to bootstrap borrow demand and initial deposit rate stability. The protocol distributes ANC tokens every block to stablecoin borrowers, proportional to the amount borrowed.

When the yield from bAsset rewards and borrow interest is less than the target rate (currently 20.5%), ANC incentives to borrowers increase by 50% every week until equilibrium is reached.

When the total yield is higher than the target rate, ANC incentives drop by 15% every week. This provides a lever by which Anchor can increase or decrease borrowing activity.